Details Are Part of Our Difference

David Booth on How to Choose an Advisor

20 Years. 20 Lessons. Still Taking the Long View.

Making the Short List: Citywire Highlights Our Research-Driven Approach

The Tax Law Changed. Our Approach Hasn’t.

Tag: Evidence-Based Investing

More Long View, More Long Term Success

Tune Out the Noise. Stay the Course.

We’re more plugged in than ever. The average person now spends nearly four hours on their smartphone daily, and over half of Americans get their news from social media. That’s a lot of headlines, and most of them short, urgent, and emotionally charged.

While access to information has never been greater, trying to beat the market by reacting to it is one of the surest ways to undermine your financial progress.

This constant stream of information can rattle even disciplined investors. Markets dip on geopolitical tensions. Another AI company announces a breakthrough. Interest rates nudge higher. The instinct is to react, shift allocations, “de-risk,” or step out of the market altogether.

But history shows that these short-term decisions often hurt long-term results.

Explore the Research

Independent research backs this up. Morningstar’s Mind the Gap study, most recently updated in 2023, compares the returns of investment funds to the returns earned by the investors in those funds. The results reveal a persistent gap: investors tend to underperform their own investments by 1.0% to 1.7% annually. Why? Because they often buy high, sell low, and attempt to time the market, frequently in response to short-term news.*

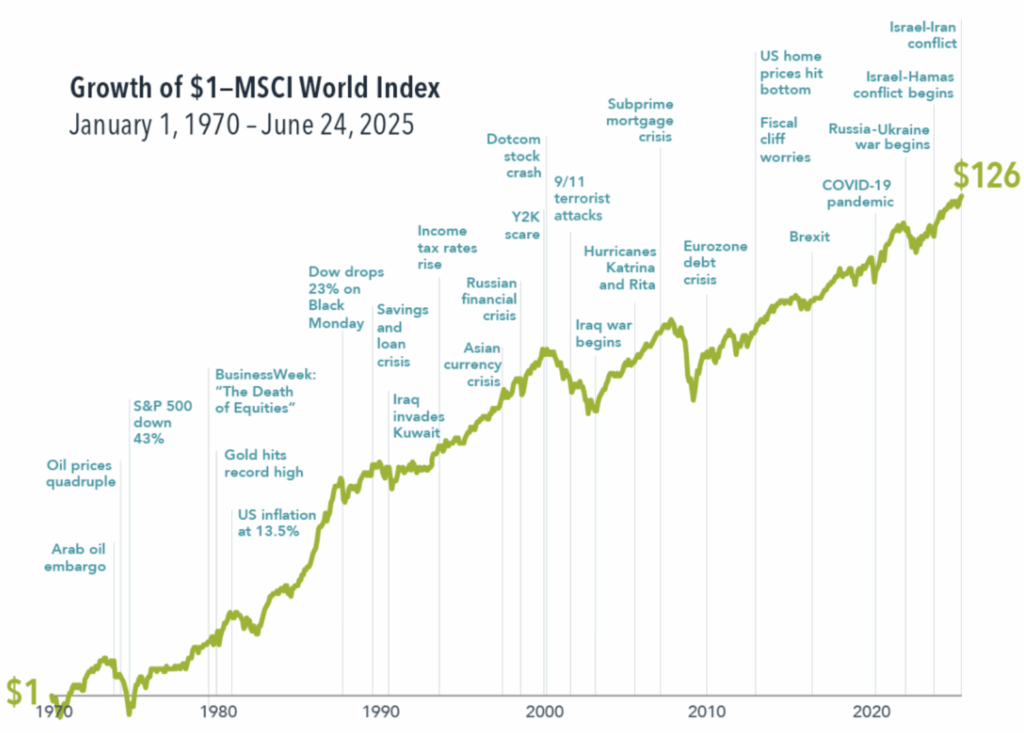

Consider this hypothetical example: Over the last 50 years (1974–2023), while markets faced double-digit inflation, multiple financial crises, and a global pandemic, long-term investors who stayed disciplined were rewarded. A $1 investment in the MSCI World Index would have grown to approximately $126.** Now imagine an investor who underperformed that index by just 1% annually; they would have ended up with a portfolio roughly 40% smaller.

What We Focus On

At Hill Investment Group, we work to tune out short-term noise, not because we’re ignoring reality, but because we believe markets are constantly processing new information. The headlines you’re reading? The market read them about five seconds ago. By the time most investors can react, they’re already behind.

Taking the Long View means focusing on what can actually be controlled: strategic asset allocation, disciplined rebalancing, thoughtful tax management, and investor behavior. That’s where meaningful long-term impact happens.

When headlines get loud, remember this: staying invested is not a passive decision. It’s an active commitment to your plan. That’s what we help our clients do every day.

That’s The Long View.

* Morningstar (2023): Mind the Gap Study – U.S. Edition

** Dimensional Fund Advisors (2025): Geopolitical Jitters

Signal vs. Noise: Cutting Through the Clutter of Financial Advice Online

It’s never been easier or more overwhelming to get financial advice. Open your phone and you’ll likely see someone with a large following and bold opinions telling you what to do next with your money. Scroll your feed and it’s hard to miss: dramatic predictions, attention-grabbing “can’t-miss” trades, and influencers claiming to decode the secrets of building wealth.

Welcome to the age of the “finfluencer.” While some have genuine experience, many are focused on views, and not your best interest.

At Hill Investment Group, we believe that real advice should be simple, clear, and grounded in evidence, not hype. That’s why we’re launching a new series to unpack misleading ideas that circulate online or in print.

Our goal? To inform, not entertain. To offer substance, not speculation.

We won’t chase the latest trend. We’ll challenge it with patience, perspective, and real-world research. That’s because, when it comes to your financial future, having a long-term plan that is built on decades of data and thoughtful execution matters more than a viral headline.

We hope this series gives you and those you care about a steady hand in a noisy world. We’ll start next month with one of the most common (and flawed) ideas making the rounds today.

Heard something at work, at golf, or on social media that has you asking, “Should I be paying attention to this?”

Feel free to share it with us. We’d love to help unpack it. Submissions will remain confidential unless we get your permission to share anonymously. Send to: zenz@hillinvestmentgroup.com

Please note: Submissions are reviewed for educational purposes only and do not constitute personalized investment advice.

20 Years of Taking the Long View

This month marks 20 years since we opened Hill Investment Group on June 6, 2005. What began as a bold idea between two friends has grown into a boutique firm serving clients in 34 states, with over $1 billion in assets under management (as of June 2025), and a talented team that now stretches from San Diego to Brooklyn.

It’s a milestone we’re proud of, and yet, we feel like we’re just hitting our stride. Our ambition today remains the same as it was at the outset: to become the leading boutique evidence-based firm in the country. That means earning your trust every day, guiding you through market swings, and standing with you through the milestones that matter most.

We’ll be celebrating this anniversary throughout the year, with reflections, lessons learned, and maybe even a few fun (non-investment!) predictions about what’s to come. If you’d like to hear how it all started, listen to this 2019 podcast episode where Rick Hill and I revisit our early days.

And here’s a favorite image from our recent team and family gathering—a reminder that what we’re building isn’t just a firm, but a community grounded in shared values and complementary skills.

Thank you for the continued trust you place in us. It’s a responsibility we’re honored to uphold.