Details Are Part of Our Difference

Embracing the Evidence at Anheuser-Busch – Mid 1980s

529 Best Practices

David Booth on How to Choose an Advisor

The One Minute Audio Clip You Need to Hear

Things Helped By Worry

Worry is a terrible strategy for solving problems.

But I have a confession to make: for a very long time, it was the only one I knew.

For example, each time I wrote a column for The New York Times, I was worried my editor would say, “Sorry, Carl, this just isn’t very good, I’m afraid that is the end of the Sketch Guy.” And then I would have to crawl under a rock, never to be heard from again.

I would bring my worries to my business partner (AKA wife). I would go on and on about, “What are we going to do if this happens?!” And when she seemed totally calm, I would say, “Aren’t you worried?!”

Because she’s generally unflappable, she would say, “I could be, if you want me to be, but I don’t see how it would help.”

It might feel like worrying helps. But as Shantideva put it:

“If you can solve your problem, then what is the need of worrying? If you can’t solve it, then what is the use of worrying?”

Worrying endlessly about something that may or may not happen in the future doesn’t help. But making a plan for what to do if that thing comes to pass does.

So now, when I catch myself starting to worry—which is often—I try to sit down and make a plan. And then I take that plan, file it away, and stop thinking about it.

That’s it. I don’t need to worry about that scenario anymore, because I have a plan.

Next time you find yourself in one of those cycles of worry, remember what Shantideva said. Action is a strategy, worry is not. So make a plan, put it away for safekeeping, and get back to work.

New Video – Buddy Reisinger

Walter “Buddy” Reisinger may just be one of the most interesting people at Hill Investment Group. His family has deep roots in the iconic beer company Anheuser-Busch. Buddy worked at the brewery after graduating from Princeton, and then UCLA for his MBA. His late mother created the famous Vivienne salad dressing which was bottled and sold coast to coast. Buddy had a beloved pet potbelly pig, his go-to karaoke song is “Come Sail Away,” and he secretly wishes he could be a DJ on a classic rock radio station. All that and he’s crazy smart with a kind heart. You’ll see a bit of that here in his video where he talks about what got him to become a fiduciary advisor and what keeps him here serving you. Enjoy.

Please also join us in congratulating Buddy on his first hole in one he sank this month!

Details Are Part of Our Difference

As our clients know, we seek to eke out every last basis point of potential return for you. So, while we balance the ideal combination of factors to achieve the highest odds of excess return, we also seek to minimize all costs, expenses, and taxes which eat into an investor’s net return. There are a couple of ways this plays out:

Evaluating Asset Managers

When evaluating asset managers, we scrutinize their trading practices to implement their strategies cost-effectively. If they don’t have reasonable trading procedures, their trading costs will be higher and, ultimately, lower the return of your investment.

Reducing Trading Fees

Just like our fund managers, we want to make sure that we are trading cost-effectively to be good stewards of your hard-earned capital. The most recent step in this effort was transitioning much of our recommended portfolio from mutual funds to ETFs, mainly to eliminate fees for trading mutual funds.

At Hill Investment Group, we are not satisfied with just better; we are always working towards finding the best solution we can find for you. The change from mutual funds to ETFs is a savings win, but we were eager to take it one step further.

Eliminating Hidden Costs

You may not know that ETFs have their own unique hidden trading costs. Like stocks, ETFs trade with a bid-ask spread. That means that, for example, market makers may buy an ETF at $9.99 and sell it to another investor for $10.01. The market maker earns a nice $0.02 profit/share, and the buyer and seller pay the cost.

We wanted to make this better. So, for ETF trades of over a certain size, rather than trade on the exchange with a limited short-term supply, we deal directly with the banks. We get the banks to compete for our business and bid against each other. This can shrink and nearly eliminate the market maker’s profit. This competition and direct access yield better prices than we could otherwise get on the exchange.

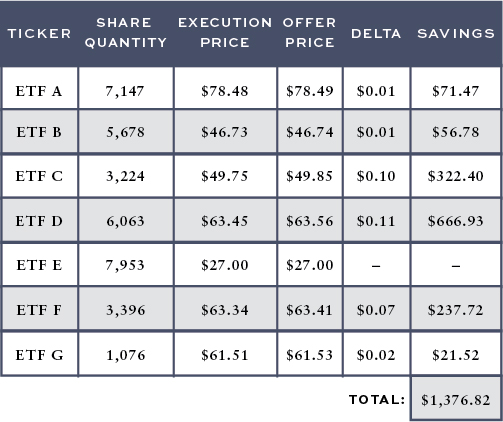

For example, we recently rebalanced one of our clients’ portfolios which resulted in purchases of various ETFs. The table above outlines the ETFs we bought, the price we would have gotten if we went to the market (Offer Price), and the price we executed at (Execution Price).

Conclusion: Details Matter

In just one day, using this trading strategy, we saved this client over $1,300 in trading costs. This one example is just one of many ways we fight for every basis point —the details matter and are part of the HIG difference.

Past results are not indicative of future results, or all client results. There are no implied guarantees or assurances that your target returns or cost savings will be the same as the example shown. Future returns or cost savings may differ significantly from the past due to many different factors. Investments involve risk and the possibility of loss of principal. The values and performance numbers represented in this report do not reflect management fees. The values used in this report were obtained from third-party sources believed to be reliable. Savings numbers were calculated by HIG using the data provided.