Details Are Part of Our Difference

Embracing the Evidence at Anheuser-Busch – Mid 1980s

529 Best Practices

David Booth on How to Choose an Advisor

The One Minute Audio Clip You Need to Hear

Category: Planning

Compounding Wisdom: Budgeting 101

This is the latest in our series of introductory “101” financial guides. Each guide reveals a set of wise actions as well as a set of behaviors to avoid. The goal? Help you make smart choices at every turn in your financial road trip. Your financial success will be exponentially enhanced when you make wise financial decisions repeatedly over a long period. This month’s focus is Budgeting, the center of your financial plan.

Compounding Wisdom: Budgeting

Compound Wisdom Actions

- Write it down – a budget is a formal, written monthly plan for your money, developed before you spend it.

- Liberate yourself – eliminate the guilt that comes with spending, knowing it was all part of the plan.

- Be patient – it takes three or four months of budgeting experience to feel confident in your plan.

- Toss the straitjacket – plan for fun, so your budget expands and doesn’t constrict your life.

- Keep it balanced – plan for all your needs, enough of your wants, and most of your savings.

- No leftovers – a zero-based budget accounts for every dollar of income, spending, and savings.

- Every dollar has a name – each dollar is either spent or saved and is assigned a category.

- Keep it simple – create a great budget with less than 20-30 categories.

- Keep track – track actual spending so you can adjust your plan for the next month as you improve.

- Minimize marital stress – it’s much easier to discuss money before it’s spent rather than after.

- Set it and forget it – using an automated tool is a painless way to plan and track your money.

Actions to Avoid

- Failing to plan is planning to fail – Don’t procrastinate; jump in, and start a monthly plan today.

- Too needy – don’t limit your budget to just the necessities – plan for family fun and relaxation too.

- What happened? – the plan has limited value if you don’t track your actual results and evaluate the plan each month or so.

- Cast it in stone – don’t treat your budget as a “read-only” document – update it often as life changes.

- Give up too soon – financial planning gets easier over time, but you must get through those first few months of learning and developing your plan.

- Mind the gap – don’t forget about planning for emergencies, gifts, vacations, large purchases, kid’s activities, and all those non-recurring one-off expenses.

Feel free to pass this along if you know someone who might benefit from the guidance and look for more from me in this monthly series.

I lead our Hillfolio level client service and planning efforts, learn more about me here and reach out if I can help you put the magic of compounding on your side.

Broken Clocks are Right Twice a Day

Does anyone know when to get in and out of the market? Many professionals try, and we’ve heard a few theories from amateur investors lately. It’s tricky to tell fact from fiction. There are a million ways to analyze historical data to find timing patterns that appear to produce attractive returns. The real question you need to ask yourself: “Is there any reason why I should expect that pattern to continue in the future, or is it purely due to chance?”

An example. Over the last thirty years, if you sorted stocks based on the letter of the alphabet they started with, you would see that stocks that began with the letter “M” outperformed those that started with the letter “E.” Is there any reason to suspect this to continue over the next 30 years?

No, clearly, the letter of the alphabet should have no impact on a company’s returns. The reason for this difference is that Microsoft was a large, successful company over this period, while Enron was a large, unsuccessful company over this period.

When working with “noisy” data, the odds that the results are evenly distributed is very small. If you roll a die six times, the odds of getting each number exactly once is tiny (1.5%). That means there is a 98.5% chance you will roll some number two or more times and some number zero times.

A typical market timing strategy we hear about around this time of year is to “avoid investing in the month of September.” At first thought, it seems odd that September would produce below-average returns, but when you look at the historical data, it is true!

Is there any economic rationale as to why this should continue in the future? I can’t think of any. Some claim that it is due to market participants selling positions to clean up their books after taking time off in the summer. If that were true, why wouldn’t investors try and get ahead of it and sell in August? Or why wouldn’t hedge funds gobble up all the low-priced stocks and keep prices stable?

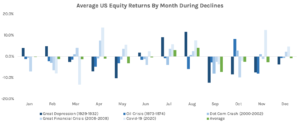

Let’s dive deeper into the data and look at the five largest market declines over the last 100 years. Each drop produced several months of negative returns, but all five of them spanned September at some point.

The recession peaked in different months every time, and every month was hit negatively at some point. However, there was bound to be one month affected more than others. It just happened to be September. From 1926 to 2021, 52% of the September months had positive returns. The large negative returns from a few market downturns have skewed the average to be negative. The question is, do we expect this to continue in the future?

Whenever you hear of these market timing strategies, you need to ask yourself if there is a logical economic rationale as to why the trend existed in the past and why it should continue in the future. Is there some risk associated with September we don’t know about? Is there some behavioral rationale that investors can’t arbitrage away? If you can’t come up with a concrete reason, whatever anomaly you are looking at is most likely due to chance and not a reliable trading strategy to implement in the future. Before accepting any investment truism, it is important to be sufficiently skeptical before implementing it yourself.

Returns from Fama/French CRSP Data Library.

Roth Conversion Perfect Storm

As of today, general equity markets are ~10-20% off their peak, tax rates are relatively low, and there are record amounts of cash on the sideline. This combination of variables presents an excellent opportunity for a strategy known as a Roth Conversion. A Roth Conversion is the process by which you take money in a pre-tax account (e.g. traditional IRA) and convert it to an after-tax account (e.g. Roth IRA). The potential benefits of such a change include:

- Tax-free growth inside the Roth IRA

- Tax-free distributions from the Roth IRA

- Avoiding required minimum distributions until you (or possibly you and your spouse) pass away

- Lower estate taxes

- Lower surcharges on Medicare premiums

For more information on Roth conversions, see the paper we created to provide more detail on this strategy, as well as the pros and cons of Roth conversions.

While this all sounds great, and it is, to receive these benefits, you have to pay ordinary income taxes at the time of conversion. This is a strategy worth considering if you are in a relatively low tax bracket because you recently retired and haven’t yet started receiving your Social Security or taking required minimum distributions. Even if you are in a higher tax bracket, it could still make sense because we could implement other tax strategies simultaneously. If you’d like to know the specifics around this strategy or any different ways we help clients maximize their long-term odds of success, we’d be happy to talk with you.