Details Are Part of Our Difference

Embracing the Evidence at Anheuser-Busch – Mid 1980s

529 Best Practices

David Booth on How to Choose an Advisor

The One Minute Audio Clip You Need to Hear

Category: Education

Hey Hill, how can I…

At Hill Investment Group, we recognize that when a few clients raise the same question, it’s likely that more have similar thoughts. To better serve you, we’re introducing a new segment in our newsletter where we’ll address common questions and how we approach them. To submit questions for future newsletters, email us at info@hillinvestmentgroup.com

Hey Hill, what should I do about 401k accounts with previous employers?

Congratulations! You just started a new job that provides fulfillment, purpose, and great rewards. In your initial weeks, your new employer offers you a new retirement plan with wonderful investment options and a generous company match.

What can you do to maximize the value of your current retirement plan as a part of your overall portfolio? What about the employer retirement plan you left behind with your previous job?

For your current plan:

- We can incorporate your retirement plan assets into your overall plan and portfolio. This helps us stay in line with your goals and can help with after-tax returns. You can find more details here.

For the plan you left behind with your previous job:

You have four basic options:

- Leave the money in your old employer’s plan. (Usually not a great idea.)

- Transfer the funds into your new employer’s plan.

- Transfer the funds into your existing IRA (traditional and/or Roth).

- Cash-out the plan and pay the taxes and penalties, if applicable.

Here are some key factors that may influence your decision:

- Employer plans have a set menu of investment options and associated fees. While you may be satisfied with those options, a rollover IRA will not limit investment options and generally allows you to invest at a lower cost.

- Many who hold on to old employer plans tend to lose track of them; therefore, they are rarely rebalanced as the market changes nor managed as part of their household portfolio.

- Many plans have pre-tax and Roth components, which may or may not align with a new employer’s plan offerings, but they can be easily rolled over to your traditional and Roth IRAs.

- Cashing out of the plan may involve unnecessary penalties and taxes.

- A unique feature of a 401k is that you can borrow money against it but not from an IRA.

- If you utilize a Backdoor Roth strategy, you may prefer to keep your retirement funds in a 401k to avoid the complications of a non-zero balance IRA account.

In the end, the combination of the above factors leads many to roll over their old plan to their individual IRA. This IRA becomes a hub as they move in and out of employers’ plans throughout their careers. On balance, the ability to choose your low-cost investment options in harmony with your other assets makes the option to roll over into an IRA a sound decision.

Anytime you change jobs, we encourage you to discuss your situation with your Hill advisor. One size doesn’t fit all, and your advisor can help you work through your situation. Book a call with us if you have questions!

Hill Investment Group is a registered investment adviser. Registration of an Investment Advisor does not imply any level of skill or training. This information is educational and does not intend to make an offer for the sale of any specific securities, investments, or strategies. Investments involve risk, and past performance is not indicative of future performance. Return will be reduced by advisory fees and any other expenses incurred in managing a client’s account. Consult with a qualified financial adviser before implementing any investment or financial planning strategy.

The Bumpy Road

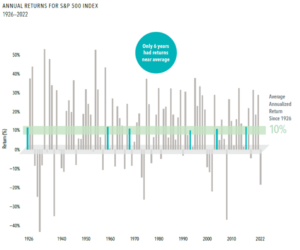

Historically, the US Equity market has returned about 10% annually to investors from 1926 – 2022. Due to this historical rate of return, many investors expect this level of return year over year. However, stock markets are highly volatile. Although the average is 10% per year, it is extremely rare for the market to be up 10% over any given year.

Since 1927, there have only been 6 years where the stock market returned between 8-12%. Thus, even though you should expect the market to give you a 10% return, you should expect the market over any given year to hardly ever give you a 10% return. It is this bumpy road that creates the risk in investing in equities, which is why you are compensated with the 10% annual average return. The key is to take the long view and not look at quarter-to-quarter or year-to-year returns.

People often panic when their expectations don’t match reality. Investors expect a 10% return every year, which will often not materialize. When the market goes down and does not match this 10% expectation, investors tend to panic. Changing your expectations on the range of outcomes of equities while keeping in mind the long-term average can help investors stick to their plan.

Hill Investment Group is a registered investment adviser. Registration of an Investment Advisor does not imply any level of skill or training. This information is educational and does not intend to make an offer for the sale of any specific securities, investments, or strategies. Investments involve risk, and past performance is not indicative of future performance. Return will be reduced by advisory fees and any other expenses incurred in managing a client’s account. Consult with a qualified financial adviser before implementing any investment strategy.

Hill Investment Group may discuss and display charts, graphs, and formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used alone to make investment decisions.

Keep It Simple

At conferences, I often hear experts advocate for private and alternative investments, claiming they’re essential for our largest and most sophisticated clients. They argue that these exclusive opportunities are what the wealthy truly want. These voices are growing louder, and the products they pitch are becoming more prevalent.

At Hill Investment Group, we take a different approach. We continue to value simplicity and transparency, regardless of how much money our clients have. We avoid complex, illiquid, and expensive options, even when others say they’re necessary. Our guiding question is this: once the marginal utility of wealth kicks in—when each additional dollar has less impact on your life—why take on added risks?

You can achieve extraordinary success by embracing what we call a “passive-aggressive” approach:

- Own global capitalism: Invest in broad market ETFs.

- Tilt toward premiums: Focus on factors identified by research to enhance returns.

- Rebalance regularly: Sell what’s done well, buy what’s lagged.

- Tax loss harvest: Capture losses to offset gains.

- Let it compound: Give your investments time to grow.

- Keep investing: Stay committed over the long term.

- Ignore the noise: Focus on your strategy, not the headlines.

By sticking to these principles, you can build and preserve wealth without getting caught up in the complexities that others might push.

Keep it simple!